Still using genetic data? A comparative review of Canadian life insurance application forms before and after the GNDA

Abstract

Genetic testing's increased availability has raised concerns about “genetic discrimination” (GD), where individuals may face unfair treatment, particularly when purchasing personal insurance, because of their genetic characteristics. In 2017, Canada passed the Genetic Non-Discrimination Act (GNDA) to prevent GD. This manuscript reviews post-GNDA life insurance application forms and compares them with pre-2014 application forms to assess the impact of the GNDA on insurance practices in Canada. Based on our comparative assessment, we found that the GNDA has had a modest impact on the practice of life insurers in Canada. Our study also confirms that questions about family history of disease and broadly formulated inquiries are still used on life insurance application forms. Both can, in the absence of clear instructions, lead applicants to disclose protected genetic information.

Introduction

Underwriting is the cornerstone of the Canadian life insurance industry. In this practice, insurers evaluate an applicant's health profile to determine coverage eligibility and the cost of premiums. In the case of life insurance, an applicant's medical and lifestyle information relevant to health significantly influences underwriting decisions (Macedo 2009). In Canada, applicants are subject to the legal duty of disclosure, as insurance contracts are to follow the concept of “utmost good faith”. As clarified by the Supreme Court of Canada, the “duty of honest contractual performance” implies a risk of nullification of a contract because of “half-truths” or “omissions” made by any contractual party (Supreme Court of Canada 2020). This means applicants are responsible for disclosing any information they believe to be relevant to their state of health (Supreme Court of Canada 2020). False or incomplete declarations can result in insurance being annulled at the request of an insurer. Thus, in cases of uncertainty about its relevance, applicants are encouraged to disclose health-related information to insurers (Ashcroft 2007).

Underwriting, however, must still be considered in light of the consequences scientific advancements may have on people's lives. The rapid progress of genetic research and testing in recent years has led to rising concerns regarding genetic discrimination (GD) (Lee 1993)—especially among members of the population who are at greater risk of developing genetic diseases (Wauters and Van Hoyweghen 2016; Bombard et al. 2012; European Respiratory Society 2023). When discussing GD, it is important to understand that clinical genetic test results are generally indicative of a person's susceptibility to developing a disease in the future and are only rarely determinative (Burke 2014; Johns Hopkins Medicine 2021). Additional factors, such as the environment and lifestyle choices, may also come into play, raising concerns about the extent to which these results are really indicative of a person's health risks (Mayo Clinic 2023).

Definitions of GD can vary widely. In the context of life insurance, it can be defined as “the differential adverse treatment, or unfair profiling, of an individual relative to the rest of the population based on actual or presumed genetic/genomic information and other “omic” data” (Global Alliance for Genomics and Health 2022). For example, an individual who has tested positive for a disease like Huntington's may face important barriers to accessing life insurance or be completely excluded from an insurance pool (Adjin-Tettey 2013). According to many experts, as a result of the perceived threat of GD, higher risk individuals may refrain from undergoing medically relevant testing (Lapham et al. 1996). Such concerns may also hinder the recruitment of participants for genetic research projects (Matloff et al. 2000). In contrast, from the perspective of life insurers, access to genetic testing is necessary to avoid anti-selection (Howard 2014). Anti-selection occurs when an insurer and an applicant do not have equal access to information that is relevant for underwriting. In such instances, higher risk applicants could seek high coverage based on information about their risk status not shared with insurers. If this situation were to materialize on a large scale, there could be a risk that insurers would have to raise their insurance prices, potentially resulting in the collapse of the insurance market (Howard 2014). However, in jurisdictions where genetic test results are protected, such as France and the United Kingdom, there is no evidence of costs spiraling out of control (Klitzman et al. 2014; Golinghorst et al. 2022).

Despite the passage of non-discrimination laws in other European and North American countries, like the Genetic Information Non-Discrimination Act in the United States (2008) and the German Genetic Diagnosis Act (Gendiagnostikgesetz, GenDG) in 2009, Canada did not adopt legal protection against GD until 2017 (Rothstein 2009). In May 2017, following a required consultation process, Canada promulgated the Genetic Non-Discrimination Act (GNDA) (Government of Canada 2017). This Act defines a genetic test as one that “analyzes DNA, RNA, or chromosomes for purposes such as the prediction of diseases or vertical transmission risks, or monitoring, diagnosis or prognosis” (art. 2). The GNDA makes it a criminal infraction to require genetic testing or genetic test result disclosure as a condition for providing an individual with goods or services (art. 7).

The GNDA prohibits the non-consensual disclosure and use of genetic test results in contractual agreements. However, it remains an open question whether, in doing so, the law achieves its purpose of preventing GD or whether dishonest or unscrupulous insurers are still accessing genetic information directly or indirectly. Are companies circumventing the GNDA? Companies may explicitly ask for genetic test results in their forms. In other instances, they may indirectly seek to obtain such information by broadly enquiring into an applicant's family history of genetic disease. Such questions are important to consider when examining the impact of the GNDA on the practices of insurance companies. It should also be noted that the GNDA's definition of genetic testing does not account for recent scientific developments such as risk prediction models that integrate polygenic risk scores and somatic or germline gene editing. Underwriting decisions have historically also included an assessment of an individual's family medical history, which is not prohibited by the GNDA. Yet, Canadians with a high risk of Huntington's disease cited disclosure of family history as the primary reason for their experiences with GD (Bombard et al. 2009).

The information requested by insurers in their application forms is a valuable indicator of whether industry has changed its practices to comply with the GNDA (Arych and Joly 2021; European Respiratory Society 2023). Importantly, these application forms are part of the insurance contract and the primary source of information received by insurers in underwriting (European Respiratory Society 2023). In 2014, 3 years before the passing of the GNDA, we reported on the level of interest of Canadian insurers in genetic information by analyzing the content of their application forms (Feze and Joly 2014). At that point, our findings showed insurance companies were seeking genetic information, mostly through indirect means, using broad inquiries and questions on family history of disease. This line of inquiry was thought to be legally permissible by many experts who believed insurers were entitled to know any information relevant to an applicant's health (Lemmens 2000). Before its passage, many stakeholders suggested the GNDA would have a game-changing effect (Huntington Society of Canada n.d.; Supreme Court of Canada 2020). They, however, disagreed on what that effect would be. While some argued the GNDA would put the commercial viability of the Canadian insurance industry at risk, others suggested that it would protect and reassure patients to take clinically indicated genetic tests and take part in genetic research (Golinghorst et al. 2022). This study aims to identify changes in the practice of the Canadian life insurance industry following the passage of the GNDA through a comparative review of life insurance application forms. It also seeks to find any “working solutions” developed by the industry to continue using genetic information for life insurance underwriting.

Methodology

To observe the impact of the GNDA on the practice of life insurance companies, we compared and contrasted data from our 2014 analysis with new data (Feze and Joly 2014). Following our 2014 research methods, we used the same inclusion and exclusion criteria and key categories for analysis. The analysis codes were modified, however, to provide greater reliability of results and were independently reviewed by two research assistants (KC and AF). Ultimately, the sample included 34 companies and 16 insurance application forms. By reviewing primary legal documents (i.e., insurance application forms), rather than secondary sources of information, this study provides much-needed data to measure the impact of the GNDA on the practices of the insurance industry.

Identification and selection of eligible life insurers

A list of insurance companies was compiled by consulting the registries used in the 2014 study (Feze and Joly 2014)—namely, Assuris (a not-for-profit organization with whom all insurance companies in Canada are required to register), the Canadian Life and Health Insurance Association (a voluntary industry association comprising 99% of Canada's life and health insurance business), and the Autorité des Marché Financiers du Québec (the financial market authority of Quebec). This list was then cross-referenced with three additional sources (LSM Insurance, Policy Advisor, and Wikipedia) to ensure the accuracy and comprehensiveness of the findings (n = 121).

We then applied a set of inclusion and exclusion criteria. Drawing upon the criteria developed in the 2014 paper, we identified eligible life insurers based on whether they had functional websites, sold individual or whole life insurance plans, and were not primarily reinsurers. We also considered their service delivery, keeping only companies that were still in business as of May 2022 and offered life insurance products to Canadians. To keep our results generalizable, we retained only the companies that did not restrict access to their services to a specific population group (e.g., members of a specific professional order or business). This approach led to the exclusion of some fraternal benefit societies, unless they were clearly open to anyone, such as Foresters, one of the investigated companies, which happens to be a fraternal organization. To further refine the list of eligible insurers, we grouped multiple entries that were found to be affiliated with the same entity, unless they used distinct insurance application forms. This process yielded 34 providers, of which we obtained 16 applications.

Application forms and data extraction

Two investigators (AF and KC) obtained the application forms using three complementary methods: (1) using a keyword search for “life insurance application form”, “proposal form”, or “documentation centre” on the identified insurers’ website (see Supplementary Materials for a full list of keywords used); (2) performing a Google Search using Google search operators such as [“insurer name” AND “application form”] (see Supplementary Materials for a full list of keywords used); and (3) if the previous two methods yielded no results, calling the consumer lines of the insurance company and following a predetermined script to inquire about the availability of relevant insurance forms. Regretfully, such calls failed to generate new forms—thus, all forms were found through steps (1) or (2).

Additional searches were performed to see if companies had a specific form related to genetic testing or disclosure of genetic testing. This was done by (1) using a keyword search on the insurer's website, using keywords such as “genetic testing” or “genetic results” and (2) using a Google search with operators such as [“insurer name” AND “genetic testing”] (see Supplementary Materials for a full list of keywords and operators used). Five forms were identified using this method.

The application forms were then assessed for relevance to ensure that they were forms for whole life insurance products. Although a total of 16 forms were identified, this is four fewer forms than in our 2014 study. This difference can be attributed to the fact that we used more rigorous selection criteria for the current study.

To cover the wide range of formats and content in the application forms, we analyzed the forms using descriptive deductive analysis and qualitative content analysis. This was done through NVivo, a qualitative data analysis computer software. Both AF and KC independently coded the forms and agreed upon a common codebook. This codebook was then utilized by a third party (EK) to convert the statistical data by compiling it into interpretable lists. This data were collected to investigate three main research questions: (1) Following the introduction of the GNDA, how do the companies’ questions about genetics, if any, compare with those identified in our 2014 paper—has the GNDA led to the introduction or removal of specific questions in the application forms? (2) Following the GNDA, are insurers specifically asking more extensive questions about family history? (3) Do application forms include other clauses that would elicit genetic data?

Results

Broad language in the testing inquiry

The way insurers inquire about medical tests is critical, as vague phrasing may lead to the unintentional disclosure of genetic test results. We found that a concerning 75% of the companies (12/16) use broad language in their testing inquiries, possibly encompassing genetic testing (see Fig. 1). One of these companies did so by way of a child rider clause, a feature that extends coverage to an insured's dependents. The company, however, explicitly indicated that its inquiry would not include genetic testing. Additionally, of the 12 companies, 100% used the term “test” without any qualifier, while others used phrases like “investigation” (33%), “exam” (17%), or “results” (8%). While any genetic test results mistakenly provided as a response to these broad questions should be discarded by insurers, there is no way to accurately assess whether this is done. Accordingly, insurance application forms should be modified to clearly stipulate that consumers need not provide genetic test results.

Fig. 1.

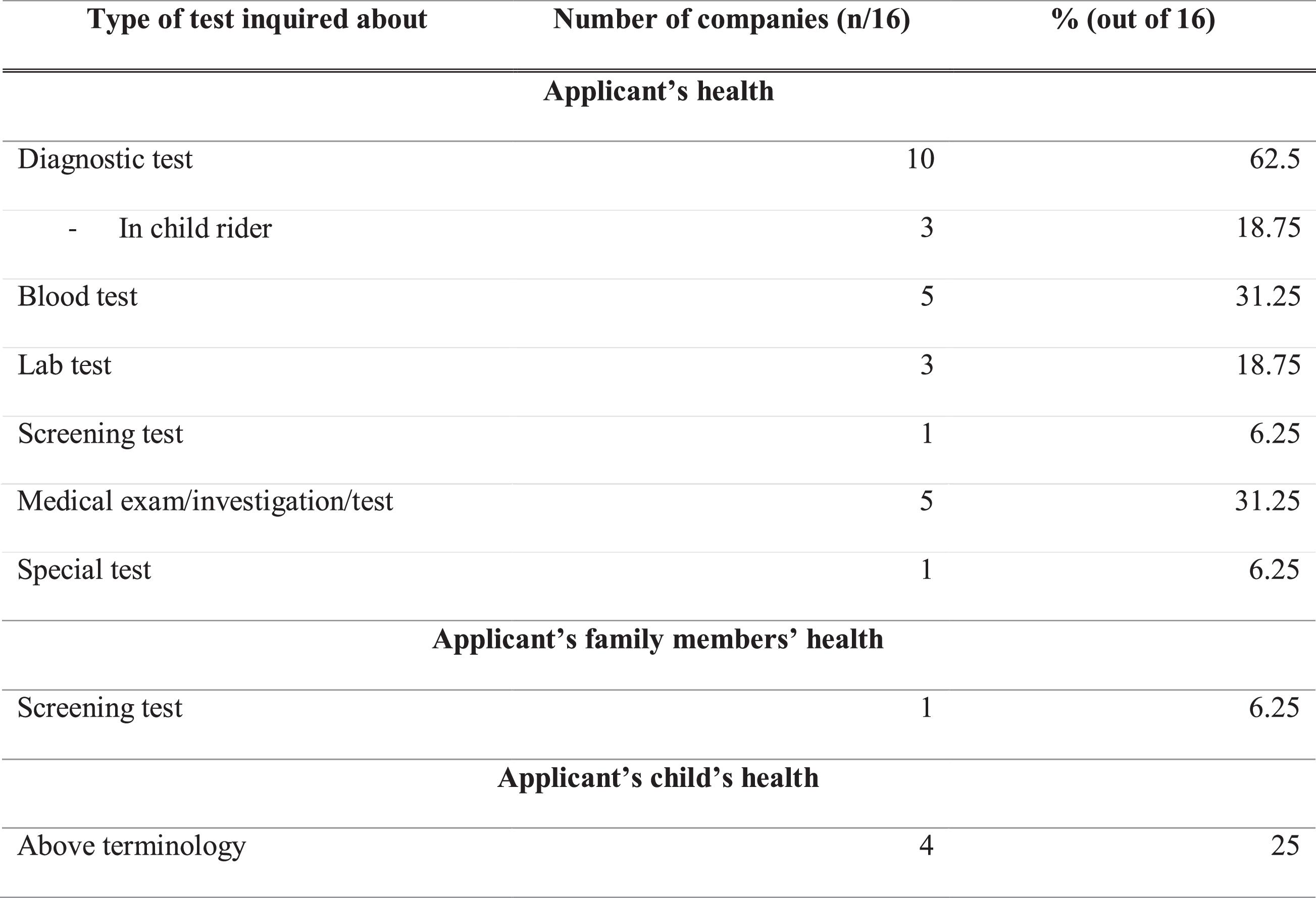

Types of testing that are inquired about

The broad qualifiers used to describe “tests” can also lead to the disclosure of genetic test results and other genetic information. Indeed, certain broad categories of tests can also be interpreted as including genetic tests. Our findings, as shown in Fig. 2, indicate that insurance providers continue to phrase their medical inquiries in very broad terms. A significant 63% (10/16) of the companies used the term “diagnostic test”, which could lead to a genetic test result disclosure. Other companies use the terms “blood test” (31%), “lab test” (19%), “screening test” (6%), or even “medical exam/investigation/test” (31%), which can all have a similar effect. Additionally, 6% (1/16) used the term “special test” with no specific detail on what “special” means and therefore could mistakenly lead to the disclosure of genetic test results. Every one of these inquiries could encompass genetic testing in their scope, which is alarming.

Fig. 2.

The problematic use of broad medical inquiries on insurance applications extends beyond applicants to include their families. Six percent (1/16) of applications used the term “screening test” in a manner that could lead to the disclosure of an applicant's family's genetic test results. An additional 25% (4/16) used the above terminology in a child rider section. For example, the child rider section in one form asks, “Has any child to be insured been prescribed any medication or had or been advised to have any treatments or diagnostic tests, whether or not completed?” This leads to the same concern about potential genetic results disclosure.

Visiting a specialist

We report that 37.5% (6/16) of the companies inquire about previous visits with a "specialist”. This term is clearly broad enough to be perceived by an applicant to include “genetic counselors” or “geneticists”. Such inquiries could then lead to the disclosure of genetic information or even genetic results protected under the GNDA. One of these six companies includes this question in a child rider section. Even if no results are provided, the disclosure of appointment(s) with a genetic professional represents a significant concern, as this type of information may not be protected by the GNDA and could lead to GD. Yet, applicants may have a legal obligation to disclose such information if asked by an insurer. A case on this matter was recently interpreted in favor of an insurance company in Denmark (Thomsen et al. 2020). While this judgment is not binding on Canadian courts, it still shows a risk that reporting information about visits to genetic specialists, when asked, could have adverse legal consequences for applicants. This highlights the complex legal landscape surrounding genetic information and the need for clearer guidelines and protections.

Concrete changes following the GNDA

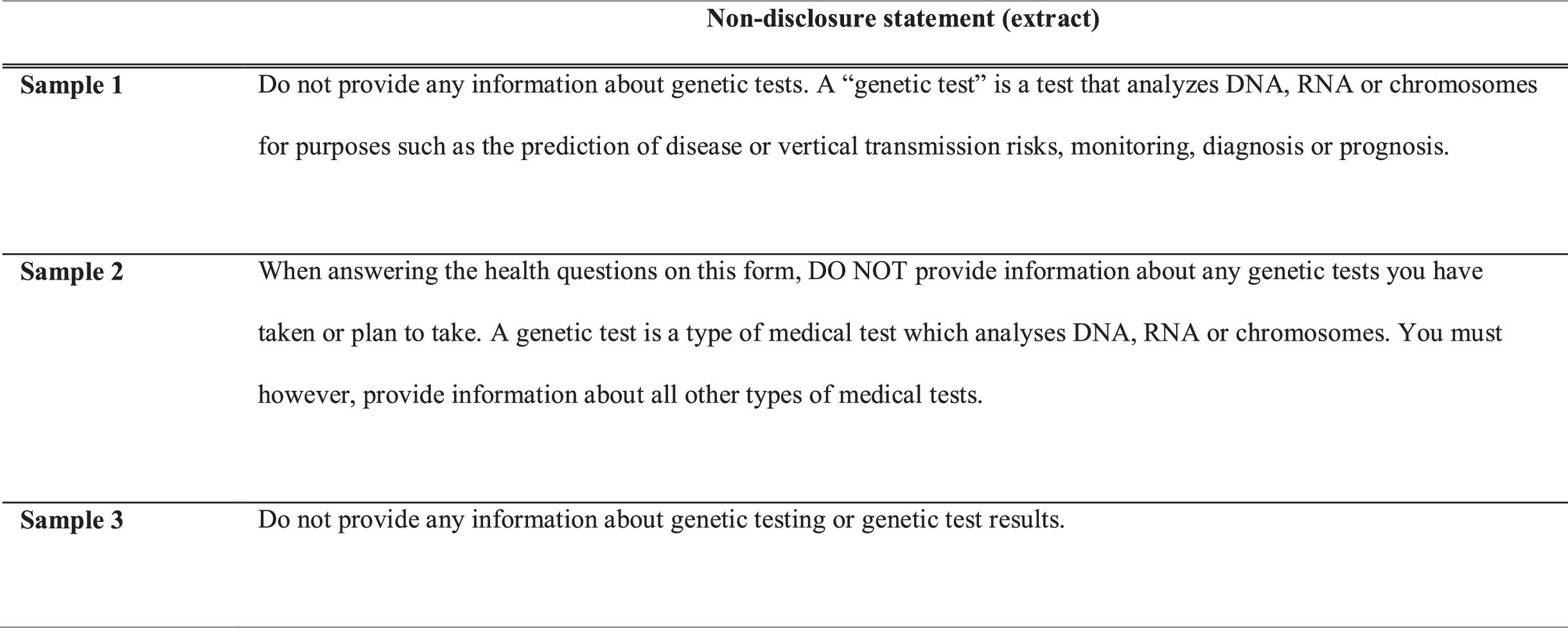

Looking at the direct impact of the GNDA, the application forms of four companies explicitly stated that applicants should not provide genetic test results. Three companies generally indicated that applicants should not provide any information about any genetic tests, while one informed applicants that it did not require them to either undergo genetic testing, or provide any genetic test information. This accounts for 25% (4/16) of the companies investigated. As such, it appears that the GNDA has had a positive impact on the Canadian life insurance industry. Notably, some companies now explicitly advise applicants not to provide genetic test results, indicating an awareness of, and a desire to conform to, the new legal requirements. This is a significant improvement from our 2014 study, which found no such indication. This practice shows how some companies are taking steps to ensure that no genetic results are mistakenly returned to them. See Fig. 3 for examples of such statements. These three samples have a similar focus and phrasing. The main difference is that some of them follow their non-disclosure statement with a definition of “genetic test”, while others do not. Indeed, 13% (2/16) of the companies also added a definition of “genetic test” in their application form—thereby providing information to the applicant. As visible in the samples reported below, the definition is very similar to the one provided by the GNDA.

Fig. 3.

Circumventing the protection of the GNDA?

Of note, amongst the companies that added a definition of “genetic test”, one explicitly clarified that applicants can include information about treatment, symptoms, complaints, or indications of a genetic condition without providing the results of a genetic test. This indicates the company's interest in circumventing the GNDA and underscores the importance of clear and precise definitions in legislation. The phrasing “It is prohibited […] to collect […] the results of a genetic test” (extracted from the GNDA) fails to address any of the information that accompanies a genetic test, such as symptoms or treatments, highlighting the need for further clarity in the regulatory framework.

Family history

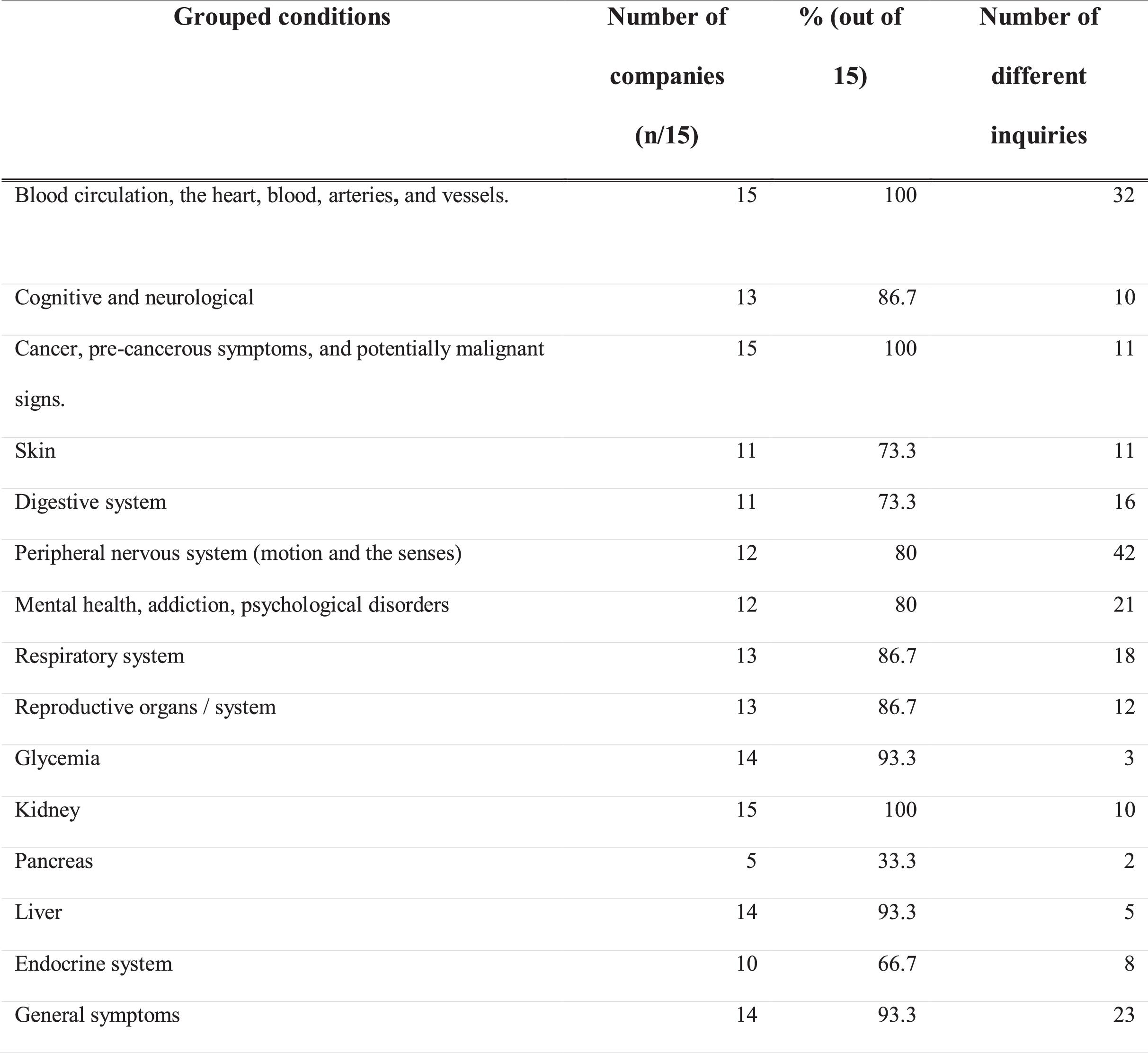

Most of the companies asked questions about family history of disease for various conditions, including tumors, heart or vascular disease, diabetes, and mental disorders. They constitute 62.5% (10/16) of the investigated companies.1 In total, 30 conditions (or sets of conditions) were inquired about.

Our research uncovered two categories of conditions that were of particular interest to a majority of insurers (89%, 8/9), that have a family history section. The first category covers a set of cognitive, neurological, and psychological conditions, including Alzheimer's disease (Richard and Amouyel 2001), dementia (Chen et al. 2009), Huntington's chorea (Conneally 1984), and alcoholism (Edenberg and Foroud 2013), all of which have a genetic component. The second is the set of “mental or nervous disorders”, many of which are also linked to susceptibility genes (National Institute of Mental Health 2020), although relevant genes for many disorders have not yet been identified and would thus not fall under the GNDA. The investigation conducted in 2014 found that 53% (9/17) of the companies inquired about Alzheimer's disease in the family history section, compared to 78% (7/9) in the present study (Feze and Joly 2014).

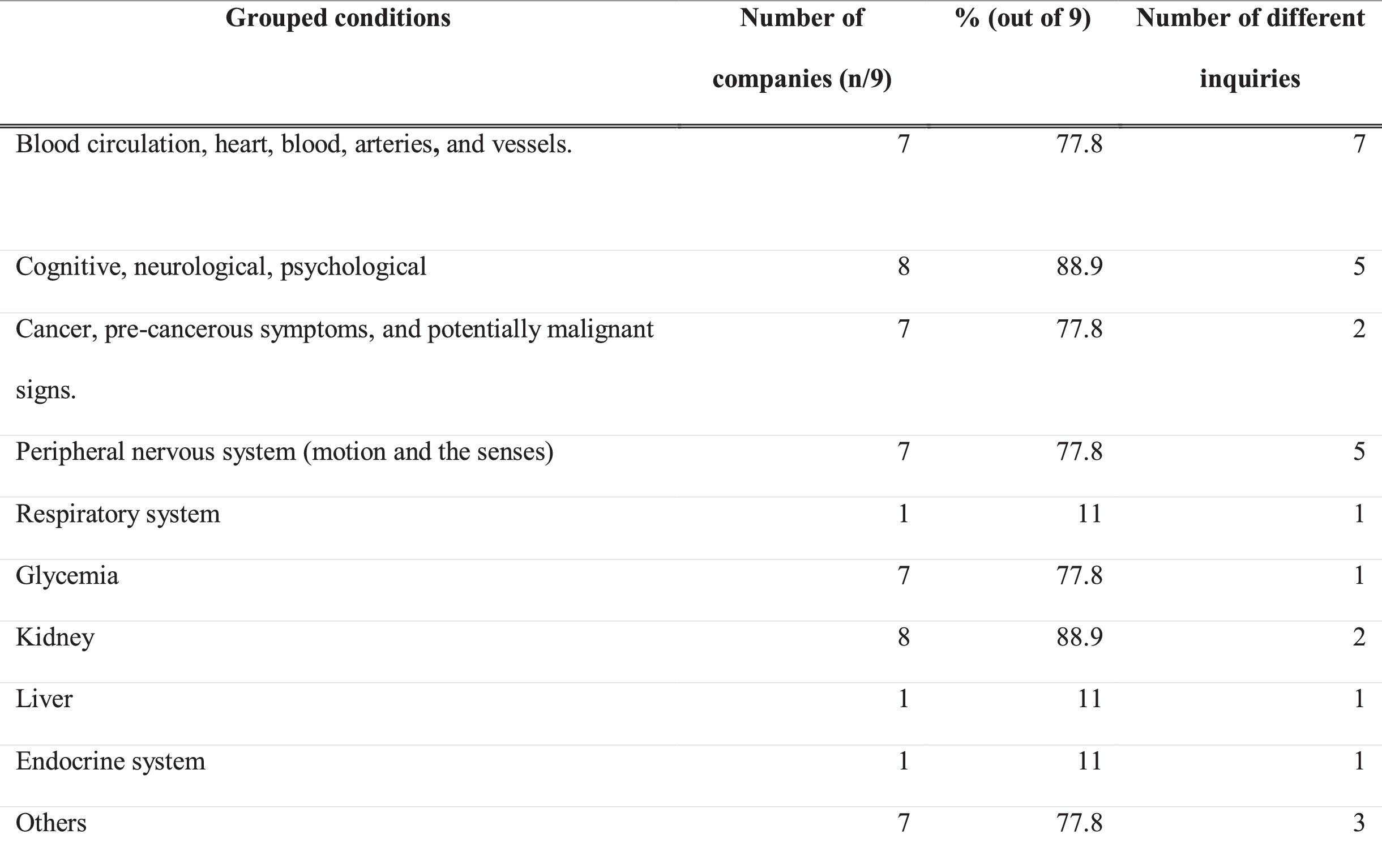

Second, kidney-related issues were also found to be prominent in the insurance forms (present in 89%, 8/9; see Fig. 4). We found that inquiries regarding polycystic kidney disease were most prominent, which is significant as this disease has been found to be a highly inheritable condition, with most cases following an autosomal dominant pattern of inheritance (Wilson 2004).

Fig. 4.

While some of the conditions inquired about remained consistently popular, others saw changes in interest over time. Indeed, the number of companies inquiring about cancer, heart disease, and Huntington's chorea decreased since 2014. On the other hand, conditions such as Alzheimer's disease, Parkinson's disease (53% in 2014 against 78% now), neuron motor disease (41% in 2014 against 56% now), and amyotrophic lateral sclerosis (35% in 2014 against 67% today) saw an increase in interest. These trends suggest that insurers are continuously adapting their inquiries to align with their risk assessments and that monitoring the evolving landscape of genetic information in insurance is crucial.

These findings also show how companies may increasingly seek to obtain genetic test results by indirectly enquiring about a person's family history. Some jurisdictions (Thomsen et al. 2020) have recognized family history as a form of protected genetic information, highlighting the ethical implications of exclusively protecting individuals with genetic predispositions identified through testing and not others (identified via family history or other means). Insurers, however, have always sought information on the familial history of disease, as it has historically been an important source of actuarial information. It is unclear, however, that protecting people with a family history of hereditary genetic conditions would positively impact participation in clinical or research genetic testing, a key objective of the GNDA (Supreme Court of Canada 2020).

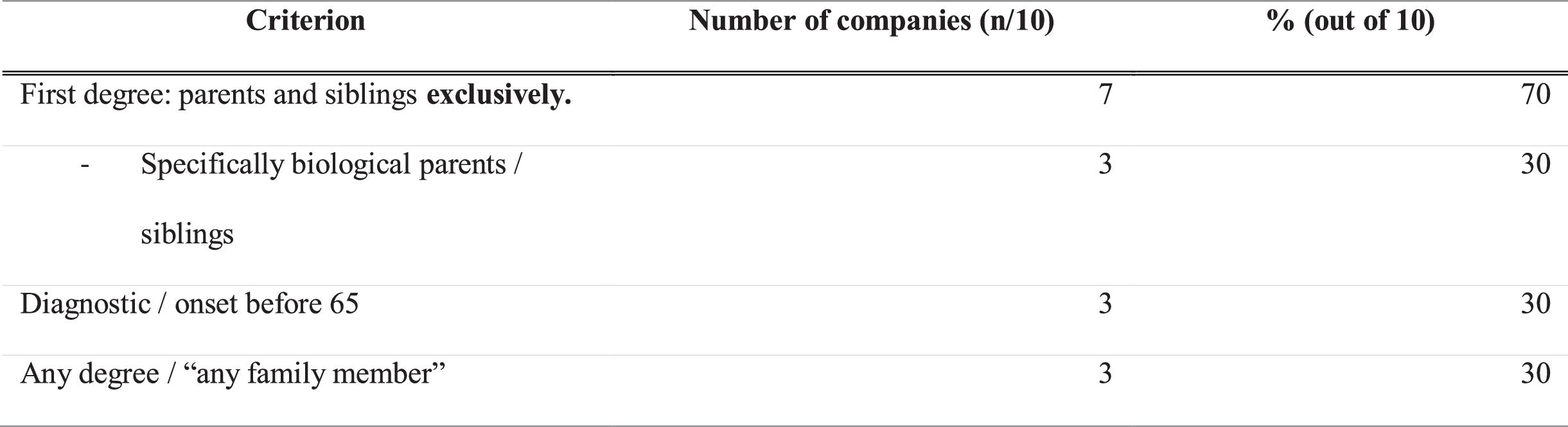

Of all the companies that asked about family history (63%, 10/16), a significant 70% (7/10) asked for history relating to family members of the first degree (parents and siblings)—while another 30% (3/10) asked about family history without specifying degree (see Fig. 5). Among the companies that inquired about members of the first degree, 43% of them (3/7) specified that said member must be biologically related to the applicant, and 43% (3/7) asked about conditions that were only diagnosed (or, in some cases, the term “onset” was used) before the age of 65.

Fig. 5.

Comparatively, in 2014, 64.7% asked about first-degree relatives and 35.3% about any degree. This shows a closeness between these proportions, with a change of less than 6% between 2014 and now.

1

Only nine of them are analyzed because one of them has a watermark across its pages, making it impossible to read the text in full.

Medical history inquiry

All companies (100%) were found to ask questions related to the applicant's personal medical history, which is to be expected on life insurance application forms. The only GD concern that arises here stems from the particular phrasing of the questions on some forms, which was reported in the above sections. Interestingly, highly penetrant monogenic conditions were less important in this section than they were in the family history section. For instance, mental health and psychological disorders—one of the two most frequent categories in the family history section—were ranked only 10th in terms of frequency in this section (see Fig. 6).

Fig. 6.

Data sharing

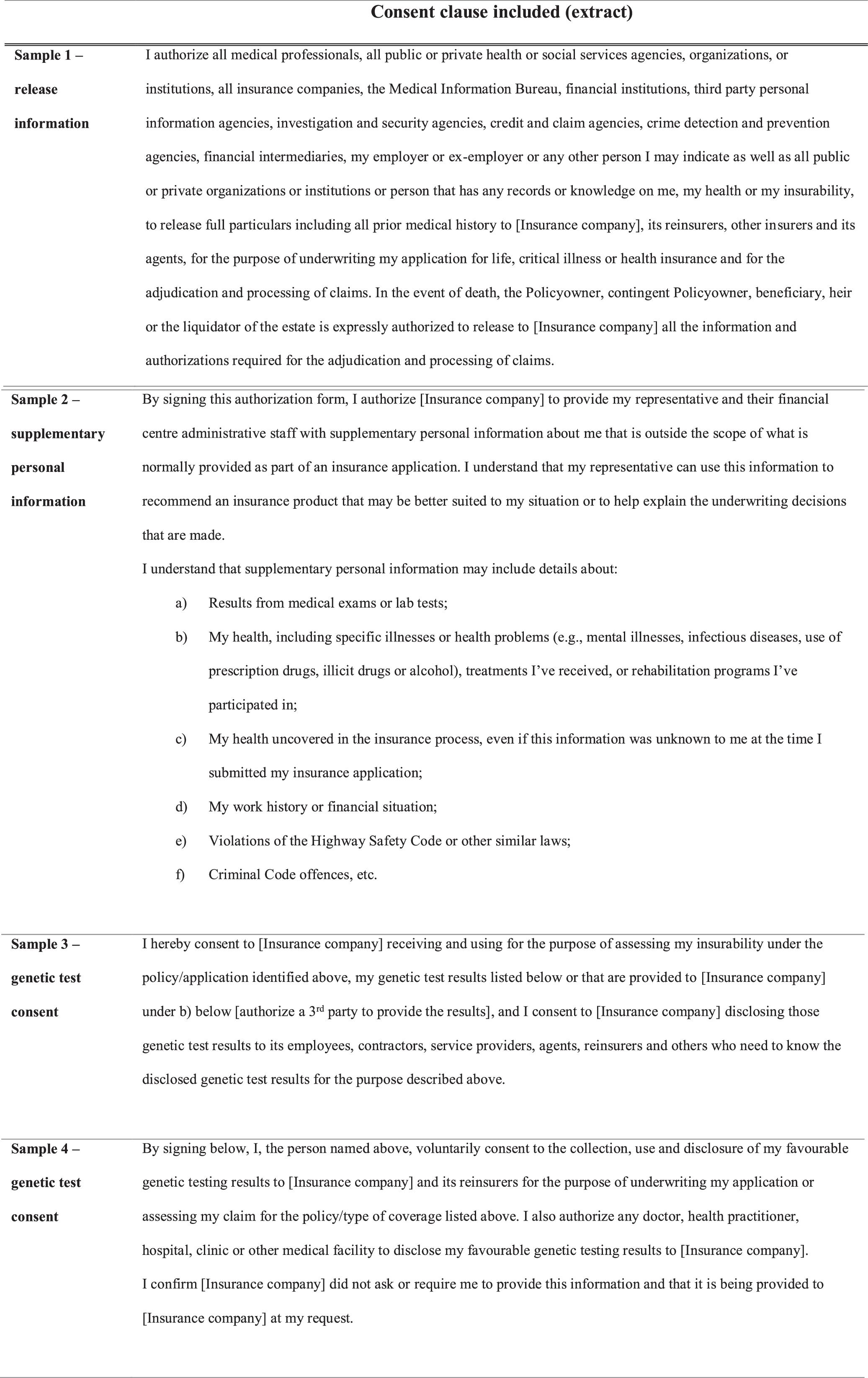

Data-sharing clauses are very common in insurance application forms. Identical to the results from our 2014 study, we found that 100% of the forms (16/16) included a data-sharing clause. Examples of such clauses are presented in Fig. 7. While the formulation of these clauses varies, they all share a common goal: seeking consent for additional information to be collected and used for underwriting purposes. Another similarity observed, between both samples, was that none of the forms specifically mentioned genetic results. This is concerning, as “genetic test results” should be explicitly excluded to avoid misinterpretation of broad expressions such as “results from medical exams or lab tests” (Sample 1) or “all medical professionals” (Sample 2) by healthcare administrators receiving requests via consent to verify data sharing clauses. Physicians may also, inadvertently, or due to lack of time, not separate genetic information from the rest of a patient's medical record. They may also feel obligated to provide such information to insurers in the absence of a specific mention to the contrary (Klitzman 2010).

Fig. 7.

In contrast to our 2014 findings, five companies were found to have added explicit consent forms to authorize their access to genetic test results. While they were likely included to facilitate the implementation of article 5 of the GNDA, they raise concerns around positive discrimination if applicants are offered lower premiums for disclosing favorable genetic test results (Government of Canada 2017). Pursuant to article 5, these consent forms are required for the use, collection, or disclosure of an applicant's test results. Samples 3 and 4 provide an example, and, while the language varies in both, they show a common objective of providing applicants an opportunity to consent to the collection of genetic test results for underwriting an application. Sample 4 specifies that this clause is voluntary, mentioning that the company does not ask for, nor requires, any genetic information to underwrite the application.

Limitations

Our manuscript aimed to gage the impact the GNDA has had on the practice of the life insurance industry by reviewing insurance application forms from Canadian insurers. It did not account for the fact that insurers may ask additional questions to further investigate or clarify what is provided on an application form. Nevertheless, companies’ standard insurance application forms are the first and most important source of information used for underwriting (Mishra 2010). Reviewing new questions and formulations used on these forms since the adoption of GNDA is a logical place to start, as it would allow our results to be used as a basis for qualitative interviews with life insurers to probe deeper into some of the more controversial practices identified.

Our sample size was limited to 16 forms. While insufficient to achieve statistical significance, this is nevertheless an impressive sample given the difficulty of obtaining information about Canadian private insurers’ underwriting practices (Rothstein 2018). This study, viewed along with our earlier 2014 research, provides a unique first look at the impact of the GNDA on Canadian life insurers’ practices. These findings should be of great importance to advocacy groups, policymakers, insurers, and economists interested in GD.

Conclusion

Our finding suggests that the GNDA has impacted the practice of the Canadian life insurance industry regarding GD. Positive changes observed include defining genetic testing (n = 2/16), explicitly telling applicants not to disclose genetic test results (n = 4/16), or, in some cases (n = 5/16), asking for explicit consent to collect and use specific genetic results. However, the generalized use of broadly phrased questions, which may be interpreted as a requirement to provide genetic results by applicants, remains a problem.

The limited scope of the GNDA and the use of broad questions by insurers also puts an onus on applicants to determine whether some genetic health information is relevant and should be disclosed. This is problematic, as a typical applicant may not understand what health information is protected, and whether they have the right to refuse disclosure. This makes the inadvertent disclosure of genetic information, including test results, a risk, rendering it impossible to assess whether insurers use this information for underwriting.

The GNDA should encourage individuals to take genetic tests without fearing a loss of their capacity to purchase life insurance. Our results raise questions about the potential need for a more comprehensive and less arbitrary scope of protection that could apply to other types of predictive health data beyond genetics. Mainly, our findings substantiate the following question: is the GD controversy symptomatic of a larger issue, one pertaining to the way private life insurance is run in Canada? This concern encompasses factors such as social inequities and the use of opaque tools and processes—an issue that goes beyond genetics and should perhaps be addressed as such.

Overall, our study shows that while the GNDA may be a positive first step in combating GD, it still suffers from important limitations and does not resolve the controversy around GD. Nonetheless, we hope this first study of the post-GNDA life insurance underwriting practices pertaining to genetic data will be helpful for all stakeholders involved in seeking policies to ensure more equitable access to life insurance in Canada.

List of abbreviations

- GNDA

- Genetic Non-Discrimination Act of 2017 (Canadian Government)

- GD

- Genetic discrimination

Acknowledgments

This research project was funded by Genome Canada.

References

Adjin-Tettey E. 2013. Potential for genetic discrimination in access to insurance: is there a dark side to increased availability of genetic information? Alberta Law Review, 577–577.

Arych M., Joly Y. 2021. Genetic discrimination in access to life insurance: does Ukrainian legislation offer sufficient protection against the adverse consequences of the genetic revolution to insurance applicants? Laws, 11(1): 2.

Ashcroft R. 2007. Should genetic information be disclosed to insurers? No. British Medical Journal, 334(7605): 1197.

Bombard Y., Palin J., Friedman J.M., Veenstra G., Creighton S., Bottorff J.L., Hayden M.R. 2012. Beyond the patient: the broader impact of genetic discrimination among individuals at risk of Huntington disease. American Journal of Medical Genetics Part B: Neuropsychiatric Genetics, 159B(2): 217–226.

Bombard Y., Veenstra G., Friedman J.M., Creighton S., Currie L., Paulsen J.S., et al. 2009. Perceptions of genetic discrimination among people at risk for Huntington's disease: a cross sectional survey. British Medical Journal, 338: b2175.

Burke W. 2014. Genetic tests: clinical validity and clinical utility. Curr. Protoc. Hum. Genet. 81: 9.15.1–9.15.8.

Chen J.-.H., Lin K.-.P., Chen Y.-.C. 2009. Risk factors for dementia. Journal of the Formosan Medical Association, 108(10): 754–764.

Conneally P.M. 1984. Huntington disease: genetics and epidemiology. American Journal of Human Genetics, 36(3): 506–526.

Edenberg H.J., Foroud T. 2013. Genetics and alcoholism. Nature Reviews. Gastroenterology & Hepatology, 10(8): 487–494.

European Respiratory Society. 2023. Genetic susceptibility. London, UK. p. 94. Available from https://www.ersnet.org/wp-content/uploads/2023/01/Major_risk_factors.pdf.

Feze I., Joly Y. 2014. Can't always get what you want? Try an indirect route you just might get what you need: a study on access to genetic data by Canadian life insurers. Current Pharmacogenomics and Personalized Medicine, 12(1): 56–64.

Global Alliance for Genomics & Health. 2022. Genetic discrimination: implications for data sharing projects. Boston, MA. pp. 1–5. Available from https://www.ga4gh.org/wp-content/uploads/Genetic-Discrimination-Dec.-2-2021.docx.pdf.

Golinghorst D., de Paor A., Joly Y., Macdonald A.S., Otlowski M., Peter R., Prince A.E.R. 2022. Anti-selection & genetic testing in insurance: an interdisciplinary perspective. The Journal of Law, Medicine & Ethics: A Journal of the American Society of Law, Medicine & Ethics, 50(1): 139–154.

Government of Canada. 2017. Genetic Non-Discrimination Act. Available from https://laws-lois.justice.gc.ca/eng/acts/G-2.5/page-1.html [accessed 12 June 2023].

Howard R. 2014. Genetic testing model: if underwriters had no access to known results. Document No. 214082. Canadian Institute of Actuaries, Canada.

Huntington Society of Canada (n.d.). Genetic discrimination and the gnda. [online]. Available from https://www.huntingtonsociety.ca/wp-content/uploads/2020/09/35-Genetic-Discrimination-and-the-GNDA.pdf [accessed 5 December 2023].

Johns Hopkins Medicine. 2021. Huntington's disease. Available from https://www.hopkinsmedicine.org/health/conditions-and-diseases/huntingtons-disease [accessed 12 September 2023].

Klitzman R. 2010. Exclusion of Genetic Information From the Medical Record. JAMA, 304: 1120.

Klitzman R., Appelbaum P.S., Chung W.K. 2014. Should life insurers have access to genetic test results? Journal of the American Medical Association, 312(18): 1855–1856.

Lapham E.V., Kozma C., Weiss J.O. 1996. Genetic discrimination: perspectives of consumers. Science, 274(5287): 621–624.

Lee C. 1993. Creating a genetic underclass: the potential for genetic discrimination by the health insurance industry. Pace Law Review, 13(1): 189. Available from https://pubmed.ncbi.nlm.nih.gov/11659744/ [accessed 12 June 2023].

Lemmens T. 2000. Selective justice, genetic discrimination, and insurance: should we single out genes in our laws? McGill Law Journal, 45: 347–412.

Macedo lionel. 2009. The role of the underwriter in insurance. Text/HTML 62506. World Bank, Washington DC. Available from https://documents.worldbank.org/en/publication/documents-reports/documentdetail [accessed 12 June 2023].

Matloff E.T., Shappell H., Brierley K., Bernhardt B.A., Mckinnon W., Peshkin B.N. 2000. What would you do? Specialists’ perspectives on cancer genetic testing, prophylactic surgery, and insurance discrimination. Journal of Clinical Oncology, 18(12): 2484–2492.

Mayo Clinic. 2023. Amniocentesis. Available from https://www.mayoclinic.org/tests-procedures/amniocentesis/about/pac-20392914 [accessed 12 September 2023].

Mishra K. 2010. Fundamentals of life insurance: theories and applications. PHI Learning Pvt. Ltd. Available from https://books.google.com/books/about/Fundamentals_Of_Life_Insurance_Theories.html?id=T3FFG8SKh1gC [accessed 12 June 2023].

National Institute of Mental Health. 2020. Looking at my genes: what can they tell me about my mental health? Available from https://www.nimh.nih.gov/health/publications/looking-at-my-genes [accessed 12 June 2023].

Richard F., Amouyel P. 2001. Genetic susceptibility factors for Alzheimer's disease. European Journal of Pharmacology, 412(1): 1–12.

Rothstein M. 2009. GINA's beauty is only skin deep. Gene Watch, 22(9): 9–12.

Rothstein M.A. 2018. Time to end the use of genetic test results in life insurance underwriting. Journal of Law, Medicine & Ethics, 46(3): 794–801.

Supreme Court of Canada 2020. Reference Re Genetic Non-Discrimination Act, Supreme Court of Canada. Available from https://www.scc-csc.ca/case-dossier/cb/2020/38478-eng.aspx [accessed 21 February 2022].

Thomsen H., Kjærulf S.M., Schmith A.B.P. 2020. Insurance & reinsurance. Chambers Global Practice, Denmark. Available from https://kammeradvokaten.dk/media/7899/chambers-insurance-and-reinsurance-denmark-as-published-_2020.pdf.

Wauters A., van Hoyweghen I. 2016. Global trends on fears and concerns of genetic discrimination: a systematic literature review. Journal of Human Genetics, 61: 275–282.

Wilson P.D. 2004. Polycystic kidney disease. New England Journal of Medicine, 350(2): 151.

Supplementary material

Supplementary Material 1 (DOCX / 12.3 KB).

- Download

- 12.37 KB

Information & Authors

Information

Published In

FACETS

Volume 9 • January 2024

Pages: 1 - 10

Editor: David Moher

History

Received: 13 June 2023

Accepted: 24 September 2023

Version of record online: 11 January 2024

Copyright

© 2024 The Author(s). This work is licensed under a Creative Commons Attribution 4.0 International License (CC BY 4.0), which permits unrestricted use, distribution, and reproduction in any medium, provided the original author(s) and source are credited.

Data Availability Statement

Data generated or analyzed during this study are provided in full within the article.

Key Words

Sections

Subjects

Authors

Author Contributions

Conceptualization: AF, KC, YJ

Data curation: AF, EK, KC

Formal analysis: EK

Writing – original draft: AF, EK

Writing – review & editing: EK, DU, YJ

Competing Interests

The authors declare there are no competing interests.

Funding Information

Metrics & Citations

Metrics

Other Metrics

Citations

Cite As

Amy Fernando, Emma Kondrup, Katherine Cheung, Diya Uberoi, and Yann Joly. 2024. Still using genetic data? A comparative review of Canadian life insurance application forms before and after the GNDA. FACETS.

9(): 1-10. https://doi.org/10.1139/facets-2023-0101

Export Citations

If you have the appropriate software installed, you can download article citation data to the citation manager of your choice. Simply select your manager software from the list below and click Download.

There are no citations for this item